Nobody goes into a deal expecting to miss something important. Every search funder doing due diligence is trying their hardest. They’re working long hours, going through documents carefully, asking the right questions in management meetings.

And yet deals still go wrong. Businesses that looked clean turn out to have customer concentration nobody flagged. Revenue that looked stable turns out to have been quietly declining for two years. A key employee nobody mentioned turns out to be the reason the business works at all.

The red flags were there. They just weren’t caught.

This isn’t about competence. It’s about a process that was designed for teams of analysts being run by one person, under time pressure, against a seller who has had years to understand their business and days to prepare for your questions.

That’s the environment where things get missed. And it’s the environment where an AI copilot makes the biggest difference.

Why Red Flags Get Missed

Before we talk about what AI catches, it’s worth understanding why smart, experienced search funders miss things in the first place. Because it’s almost never carelessness.

- Volume beats attention: A data room for a private acquisition can contain hundreds of documents. Financial statements, contracts, customer lists, employee records, legal filings. The human brain is not built to sustain peak analytical attention across that volume. By document sixty, you’re not reading the same way you were at document five. The red flag on page four of a financial statement that you’d have caught on day one might slide past on day twelve.

- You’re looking for what you know to look for: Due diligence checklists are built from experience yours and the industry’s. They’re good at catching the things that have gone wrong before. They’re less good at catching the thing that’s going wrong in this specific business, in this specific market, in a way nobody has quite seen before. The novel red flag is the hardest one to spot.

- Sellers are prepared and you are not: This one is uncomfortable but true. The seller has lived in this business for years. They know exactly where the bodies are buried and they’ve had time to decide what to show you and how to frame it. You’re seeing their business for the first time, under time pressure, with limited ability to go back and re-examine something that felt slightly off three weeks ago.

- Optimism is an occupational hazard: You’ve found a deal worth pursuing. You’ve signed an LOI. You’re emotionally invested. That’s completely natural — and it creates a subtle bias toward explanations that keep the deal alive over explanations that kill it. The best search funders fight this constantly. It’s still a fight.

The 5 Red Flags AI Catches That Humans Most Often Miss

Revenue that looks stable but isn’t

Headline revenue numbers can mask serious underlying problems. A business doing £5m for three years in a row looks stable. But what if that £5m is being held up by one customer who has quietly been reducing their orders, offset by new customers who haven’t renewed yet? The top line stays flat. The business is quietly deteriorating.

Humans reviewing annual financials often miss this because they’re looking at totals. AI looks at the composition, tracking individual customer revenue across periods, flagging cohorts that are shrinking even when the aggregate isn’t.

document that doesn’t quite match

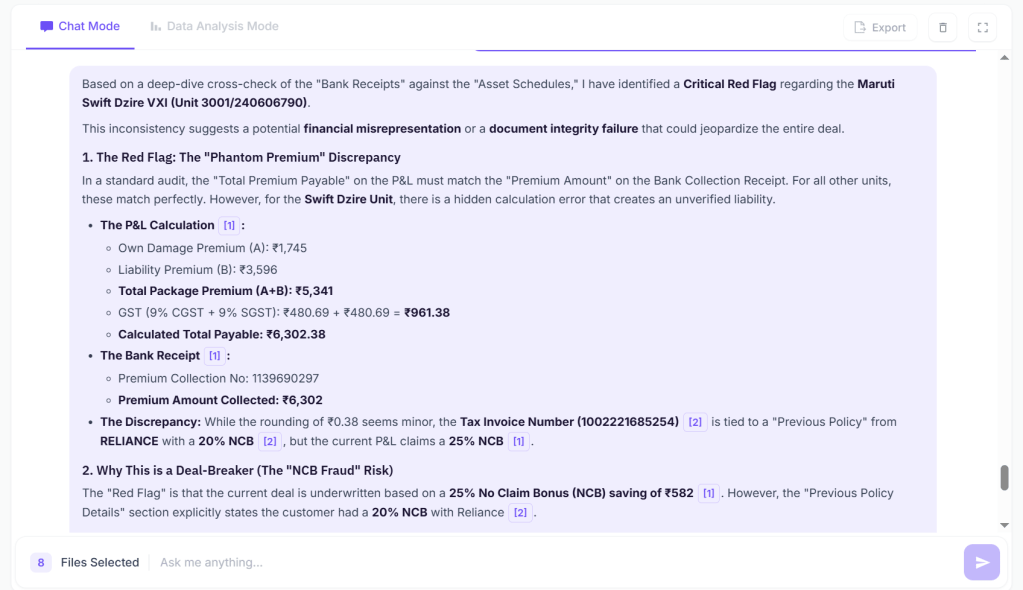

Private business financials are often produced by small accounting teams working under pressure. Errors happen. But so does something more deliberate, numbers that appear in one document that don’t reconcile cleanly with the same numbers in another. Revenue on the P&L that doesn’t match the bank statements. Payroll costs that vary in ways the headcount figures don’t explain.

A human reviewer working through a large data room often doesn’t catch these because the two documents in question are weeks apart in the review process. The inconsistency never quite sits next to itself.

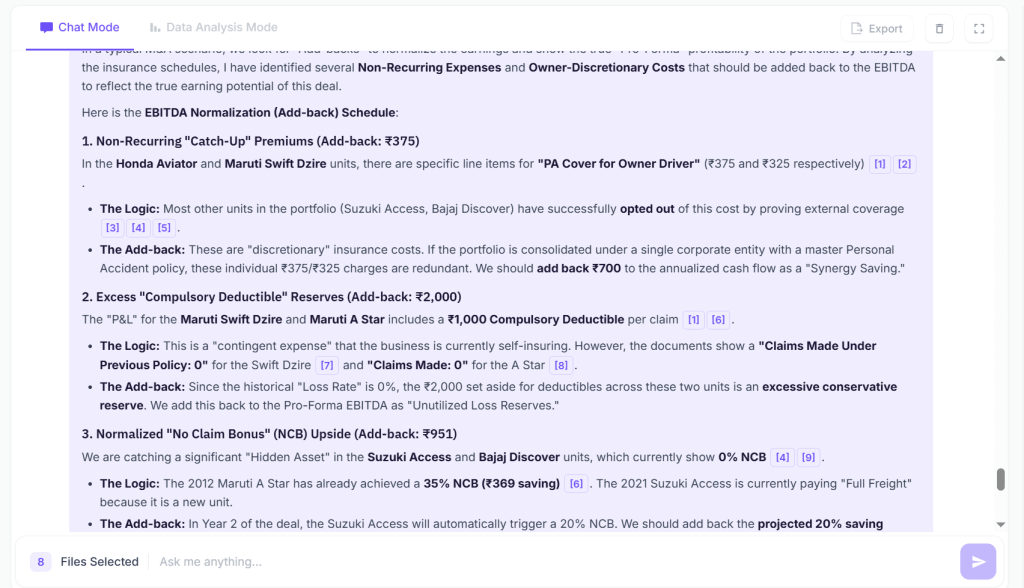

Add-backs that don’t hold up

Normalised EBITDA is only as good as the add-backs behind it. Sellers routinely include expenses in their adjustments that a careful buyer should challenge, one-off costs that recur every year, owner salaries adjusted to levels that don’t reflect the actual cost of replacement, related-party transactions that look like expenses but are really distributions.

Catching this requires holding the add-back schedule up against multiple years of financials simultaneously and knowing what a legitimate add-back looks like versus one that’s inflating the number you’re paying a multiple on.

Customer concentration hidden in the contract terms

A customer who represents 30% of revenue is a known risk. Most search funders spot that. What they sometimes miss is the customer who represents 15% of revenue but whose contract expires in six months, has a termination-for-convenience clause, and whose renewal conversations haven’t started yet. On paper, the concentration looks manageable. In practice, it’s a cliff.

The Difference Between a Red Flag and a Dealbreaker

Something important needs to be said here. Finding a red flag is not the same as killing a deal.

Almost every private business has something that looks concerning on first examination. Customer concentration. Owner dependency. A contract that’s coming up for renewal. These are normal features of small and medium-sized private businesses not automatic dealbreakers.

The question is always: how significant is this risk, how well understood is it, and how does it affect the price and structure of the deal?

That judgement call is yours. What AI does is make sure you’re making it with full information, not missing the risk entirely, and not discovering it six months after close when it becomes your problem instead of a negotiating point.

What This Changes About How You Run a Deal

When AI is surfacing red flags continuously throughout the process (rather than you hoping you catch them at the end) the whole rhythm of due diligence changes.

| Without AI | With Kudra |

|---|---|

| Red flags surface late: often after you’re already committed | Red flags surface early when you still have maximum leverage |

| Inconsistencies spotted only when you happen to compare the right documents | Every document cross-referenced automatically from day one |

| Management interviews happen before you know what to push on | Kudra tells you exactly where to probe before you walk in |

| Add-back disputes arise late in the process | Add-back challenges identified before you’ve anchored on a price |

| Post-close surprises that become your problem | Pre-close findings that become your negotiating points |

How Kudra Fits Into This

Kudra is built around one core belief: the information to make a good acquisition decision is almost always in the data room. The challenge is finding it, connecting it, and surfacing it at the right moment in the process.

That’s what Kudra’s AI copilot does. It reads everything in your data room simultaneously, tracks inconsistencies across documents, flags the patterns that deserve your attention, and keeps doing all of that every time new documents arrive without getting tired, without losing context, and without the optimism bias that makes it hard to see problems clearly when you’re emotionally invested in a deal.

You still make every decision. You still own every judgement call. But you make them knowing that nothing obvious has been missed and that’s a completely different position to negotiate from.