Evolving regulations, sophisticated fraud tactics, and aging customer records create continuous compliance challenges for financial institutions and regulated organizations. Know Your Customer (KYC) remediation ensures your existing customer database remains accurate, current, and compliant throughout the entire customer lifecycle, not just during initial onboarding.

By systematically reviewing and updating customer information, you minimize fraud exposure, satisfy stringent Anti-Money Laundering (AML) obligations, and prevent regulatory penalties. In this guide, you’ll understand what KYC remediation entails, why it’s critical, the key triggers that demand action, and a comprehensive step-by-step framework — plus how AI-powered platforms like Kudra can accelerate the process while reducing costs and errors.

What is KYC Remediation?

KYC remediation is the structured process of reviewing, updating, and validating existing customer records to ensure they remain accurate, complete, and aligned with current Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) regulations.

This ongoing compliance activity encompasses identity re-verification, document renewal for expired credentials, risk profile reassessment, and continuous monitoring to detect emerging threats. KYC remediation protects organizations from facilitating illegal activity, maintains customer trust, and helps avoid substantial regulatory fines and reputational damage.

Why KYC Remediation is Critical

Regulatory Compliance – Maintains customer records in accordance with evolving AML/KYC legislation across multiple jurisdictions.

Risk Mitigation – Dramatically reduces exposure to money laundering, terrorist financing, fraud schemes, and sanctions violations.

Current Risk Assessment – Enables precise risk scoring based on up-to-date customer information rather than outdated profiles.

Enhanced Fraud Prevention – Detects high-risk customers and suspicious patterns through systematic screening and validation.

Strengthened Customer Relationships – Demonstrates commitment to security and compliance, building long-term trust.

Penalty Avoidance – Prevents multi-million dollar fines for non-compliance with data accuracy requirements.

The primary driver for KYC remediation is regulatory compliance. Organizations that neglect systematic customer data updates face severe consequences. In 2020 alone, global AML fines exceeded 20 billion euros. Institutions discovered with outdated customer information, missing risk assessments, or inadequate monitoring face not only financial penalties but also operational restrictions and damaged reputations that can take years to rebuild.

When to Perform KYC Remediation

Risk-Based Periodic Reviews – Low-risk customers: every 24–36 months; Medium-risk: 12–24 months; High-risk: 6–12 months; Very high-risk/PEPs: quarterly or semi-annually.

Customer Profile Changes – Address relocation, name changes, occupation shifts, beneficial ownership modifications, or changes in business structure.

Regulatory Changes – New AML/KYC requirements, updated sanctions lists, enhanced jurisdiction-specific mandates, or industry guidance.

Unusual Activity or Inactivity – Large or sudden transactions, activity spikes inconsistent with profile, prolonged dormancy, or cross-border transaction patterns.

Risk Indicator Alerts – PEP identification, sanctions list matches, adverse media mentions, law enforcement inquiries, or relationship to high-risk entities.

Systemic Data Quality Issues – Database migrations, system consolidations, bulk data quality audits, or regulatory examinations revealing widespread deficiencies.

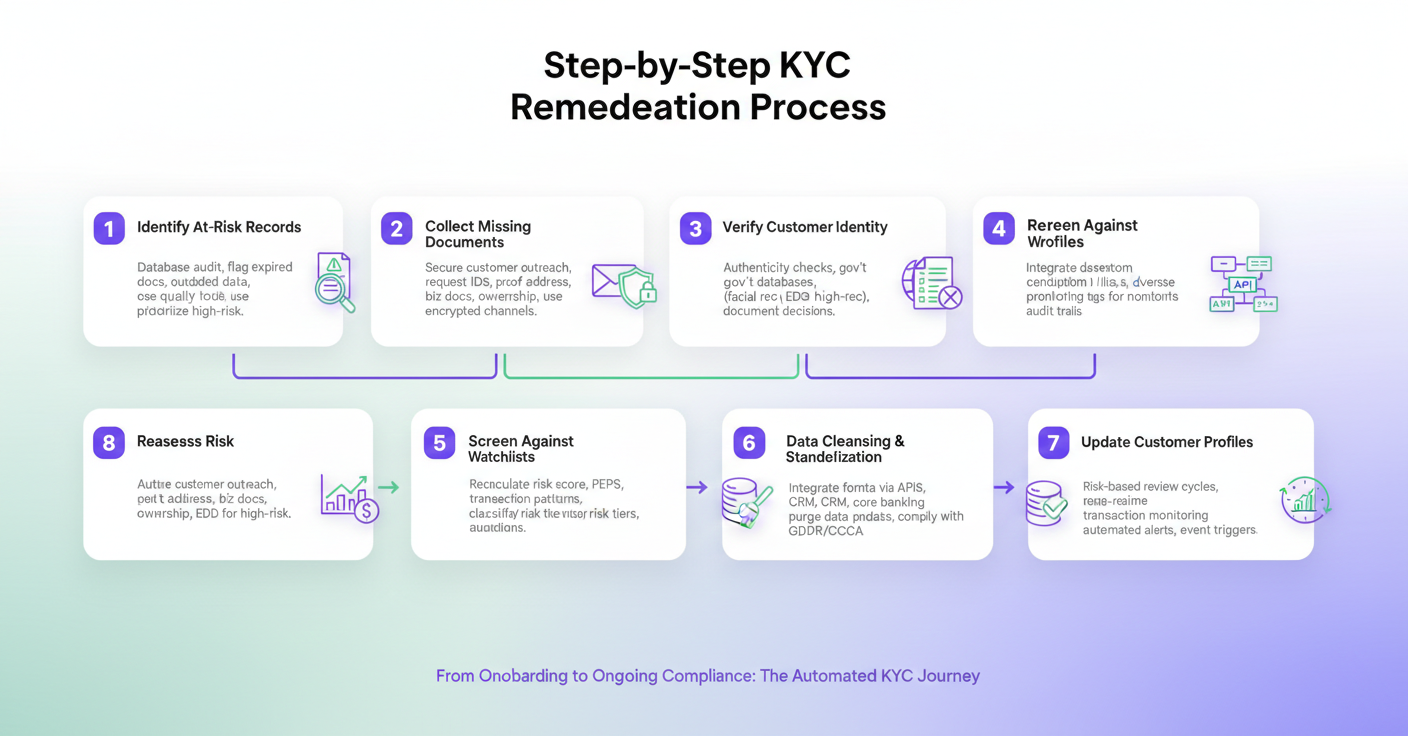

Step-by-Step KYC Remediation Process

Here is the comprehensive framework for effective KYC remediation:

Step 1: Identify At-Risk or Outdated Records

Conduct a thorough database audit to flag customer profiles requiring remediation. Target records with expired identity documents, outdated addresses, incomplete beneficial ownership information, missing source of wealth documentation, or inconsistent data across systems.

Use automated data quality tools to identify missing fields, logical inconsistencies (mismatched names or dates), duplicate profiles, and customers approaching their scheduled review date. Prioritize remediation based on risk rating, with high-risk customers, PEPs, and entities in high-risk jurisdictions receiving immediate attention.

Step 2: Collect Missing or Updated Documents

Initiate secure customer outreach to request current documentation. Required materials typically include government-issued identification (passport, national ID, driver’s license), proof of address (utility bill, bank statement, lease agreement dated within 90 days), updated business registration certificates for entities, beneficial ownership declarations, and source of funds or wealth documentation for high-risk profiles.

Implement encrypted communication channels such as secure email portals, authenticated mobile applications, or dedicated client portals to protect sensitive information. Clearly communicate regulatory obligations, submission deadlines, document requirements, and consequences of non-compliance as mandated by Customer Identification Program (CIP) regulations.

Step 3: Verify Customer Identity

Execute comprehensive authenticity checks by validating submitted documents against authoritative databases including government registries, credit bureaus, utility providers, and corporate registers. Deploy biometric verification technologies such as facial recognition comparing live selfies to photo IDs, liveness detection preventing photo or video spoofing, and fingerprint or voice recognition for high-security applications.

For elevated-risk customers, implement Enhanced Due Diligence (EDD) procedures: verify employment and income sources, confirm beneficial ownership structures through corporate filings, validate business operations and financial statements, and conduct in-depth background investigations aligning with your institution’s risk appetite and regulatory requirements.

Step 4: Screen Against PEP & Sanction Lists

Execute automated screening of updated customer profiles against comprehensive global watchlists. Key databases include the U.S. Office of Foreign Assets Control (OFAC) Specially Designated Nationals list, EU Consolidated Financial Sanctions List, UN Security Council Sanctions List, Financial Action Task Force (FATF) high-risk jurisdictions, and proprietary Politically Exposed Persons databases.

Supplement list-based screening with adverse media monitoring to identify negative news, litigation, regulatory actions, criminal investigations, or reputational concerns. Configure screening thresholds to balance detection sensitivity with false positive management, and establish clear escalation protocols for confirmed matches.

Step 5: Reassess Risk Profiles

Recalculate each customer’s risk score incorporating newly verified information, recent transaction patterns, geographic exposure changes, and regulatory environment shifts. Apply consistent Key Risk Indicators (KRIs) including transaction volume and frequency, product complexity, geographic locations, industry sector, relationship tenure, and beneficial ownership transparency.

Classify customers into appropriate risk tiers: low, medium, high, or very high risk. For customers moving to higher risk categories, adjust monitoring intensity, review frequency, transaction limits, and approval requirements. Document risk rating methodologies and decisions to demonstrate regulatory compliance and support aud it requirements.

Step 6: Data Cleansing & Standardization

Implement systematic data normalization to ensure consistency across all customer records. Standardize name formats (removing inconsistent punctuation or spacing), address structures (consistent street type abbreviations and postal codes), date formats (ISO 8601 or regional standard), and telephone numbers (international format with country codes).

Execute de-duplication algorithms to identify and merge redundant customer profiles, preventing compliance gaps and inefficient resource allocation. Correct data entry errors, remove deprecated information, and purge unnecessary data in compliance with privacy regulations such as GDPR’s data minimization principle, CCPA retention limits, and sector-specific requirements.

This cleansing ensures downstream compliance systems can reliably process, analyze, and report customer data without manual intervention or correction.

Step 7: Update Customer Profiles in Core Systems

Integrate validated and standardized data into all relevant systems via secure API connections, including Customer Relationship Management (CRM) platforms, core banking systems, transaction monitoring solutions, compliance management platforms, and regulatory reporting tools.

Implement systematic tagging and categorization: “PEP confirmed,” “EDD completed,” “High-risk jurisdiction,” “Sanctions screening passed,” or “Review due Q2 2026.” These tags trigger appropriate workflows for ongoing monitoring, transaction review, and future remediation cycles.

Maintain comprehensive audit trails documenting who updated each record, what changes were made, when updates occurred, what evidence supports changes, and which approvals were obtained. This audit capability demonstrates regulatory compliance and supports internal governance requirements.

Step 8: Implement Continuous Monitoring

Establish risk-based review cycles aligned with regulatory expectations: low-risk customers every 24–36 months, medium-risk every 12–24 months, high-risk every 6–12 months, and very high-risk customers or PEPs quarterly or semi-annually. Calendar these reviews systematically to distribute workload and prevent resource bottlenecks.

Deploy real-time transaction monitoring to detect anomalies, unusual patterns, activity inconsistent with customer profiles, or behavior suggesting money laundering or terrorist financing. Configure automated alerts tied to predefined KRIs and regulatory thresholds, enabling compliance teams to investigate immediately rather than waiting for the next scheduled review.

Integrate event-based triggers that initiate remediation outside normal cycles: sanctions list updates, PEP status changes, adverse media alerts, law enforcement inquiries, or significant transaction anomalies.

How to Automate KYC Remediation with Kudra

Automation transforms KYC remediation from a labor-intensive, error-prone manual process into an efficient, scalable, and audit-ready operation. Kudra’s AI-powered platform combines intelligent document processing, advanced data extraction, automated validation, and seamless system integration to handle the most time-consuming remediation tasks. Here is a demonstration of how to use Kudra AI:

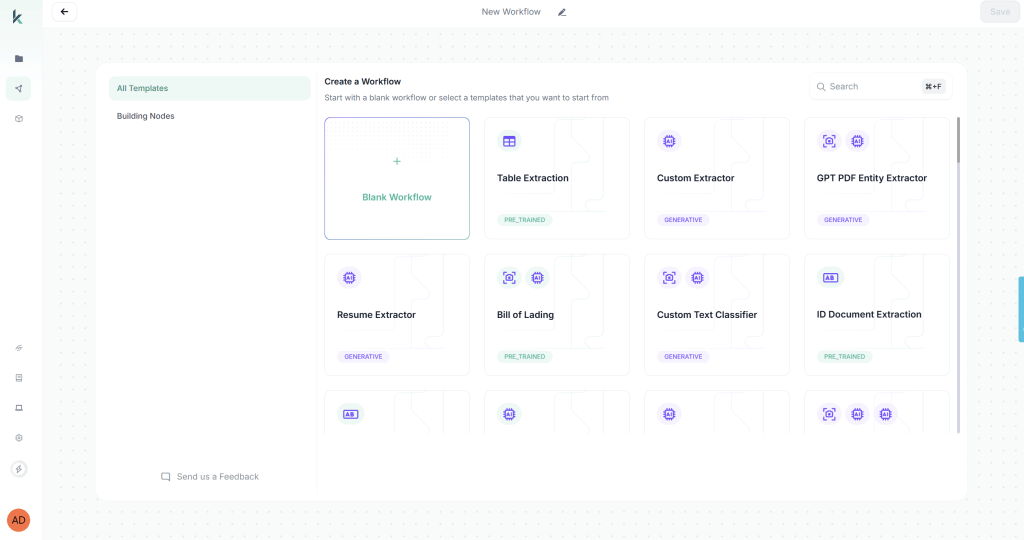

Step 1: Build the Multi-Format Document Processing Workflow

Access Kudra’s workflow builder by clicking “Create New Workflow” from the dashboard. You have two options: start from a blank workflow or use a predefined template. For this tutorial, we’ll start from scratch to demonstrate the full customization capabilities.

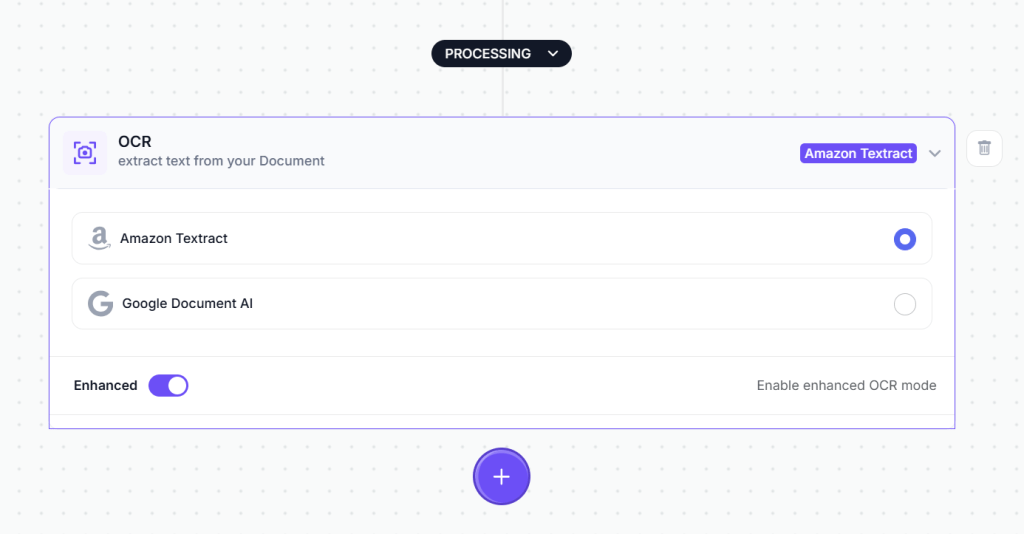

Add the OCR Component:

The first component processes the visual document and extracts raw text. From the component library, drag the OCR module onto your workflow canvas. This module handles text extraction from PDFs, scanned images, mobile photos, and any other document format you upload.

No configuration is required for the OCR component, it automatically processes whatever document format you provide.

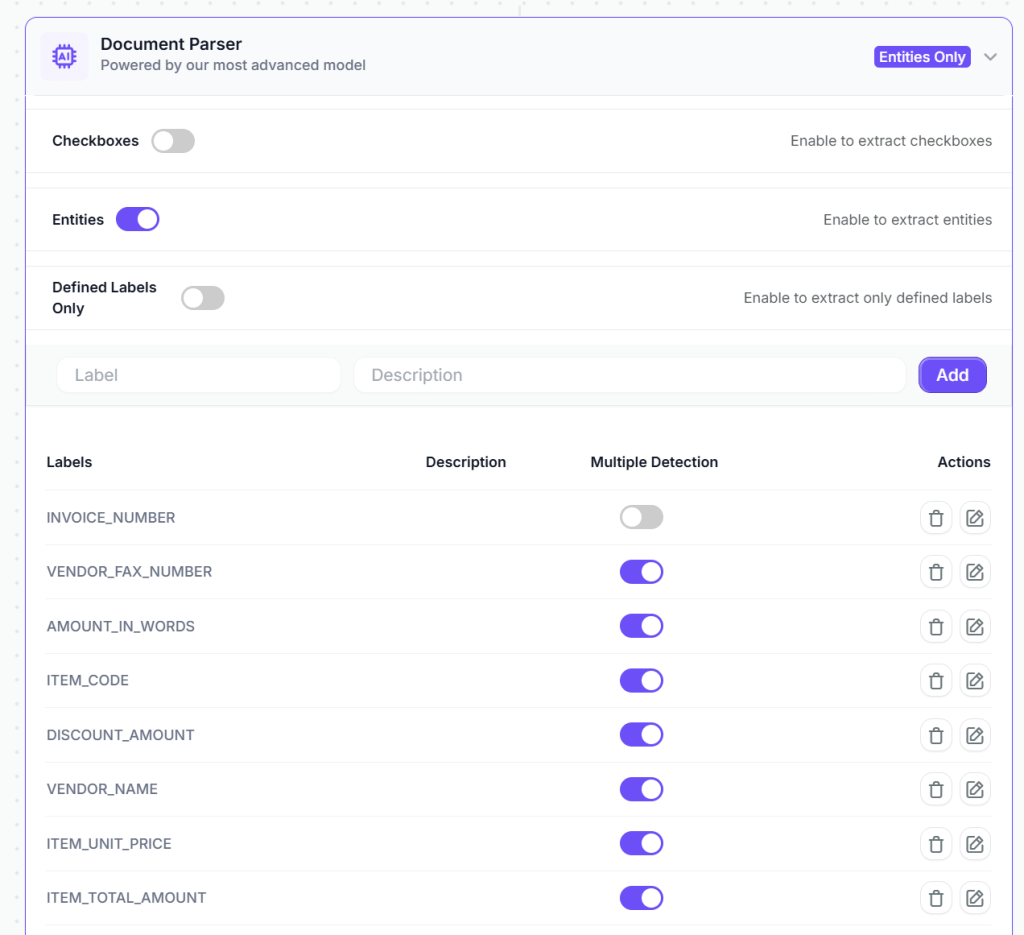

Add the Vision Language Model (VLM) Component:

Next, add a VLM component for every type of document you are working with to intelligently extract specific data fields. For example for financial statement analysis you can add a VLM to understand the structure and context, allowing it to locate relevant information regardless of document layout variations.

The VLM component in Kudra adapts to different vendor invoice formats automatically. You’re not building rigid templates that break when a vendor changes their invoice design—you’re teaching the system what information matters regardless of where it appears on the document.

Add Text Generation Component For Anything You Want To Do To Your Documents

For example to analyze your document, add a text generation component configured to act as Financial analyst. This component takes the extracted contract terms and produces a structured JSON report.

Of course, the prompt should be far more detailed than this. What you’re seeing here is only a simplified example of what you can do. Our production-ready prompts—including structure, edge-case handling, and optimization tips—are shared exclusively inside our expert community.

Inside the Slack, you’ll get free access to:

- The complete prompts we actually use in real workflows

- Explanations of why each part exists (not just copy-paste text)

- Iterations, improvements, and prompt updates as models change

- Direct discussions with practitioners building and shipping this stuff

If you want to move beyond surface-level examples and start using prompts that actually work in real systems, join the Slack and ask for a prompt. It’s free and it’s where we share the details we don’t post publicly.

Want the Full Prompt?

You can also chain multiple text generation components to create different outputs.

Each expert component outputs structured JSON that can be automatically converted into beautifully formatted outputs.

Optional: Add Post-Processing Components

Depending on your specific requirements, you can add additional data refinement steps:

Find and Replace: Standardize vendor names that appear in multiple formats. For example, invoices showing “ABC Corp” and “ABC Corporation” can be automatically matched to your vendor master database.

Format Date: Convert dates to match your accounting system requirements. This ensures consistency across international vendors using different formats (DD/MM/YYYY vs MM/DD/YYYY).

Text Transformation: Apply formatting rules such as converting account codes to uppercase, standardizing currency symbols, or making other adjustments to ensure data consistency.

Optional Post-Processing: For basic invoice processing, the VLM and validation components usually provide clean, structured data without extra steps. These additional options are available when your business logic requires them.

Configure Export Destinations

Kudra AI lets you send extracted data wherever it’s needed. Connect directly to accounting software, ERP systems, spreadsheets, databases, or automation platforms like Zapier. Multiple destinations can run at the same time, giving your team full visibility and seamless integration without manual work.

Step 4: Create a Production Project and Process at Scale

Once your workflow is ready, create a production project for your usecase. In Kudra AI, click “Create New Project” and give it a descriptive name.

During project creation, select the workflow you just built from the dropdown menu. This links your automated data extraction workflow to this specific project, meaning every document uploaded to this project will automatically be processed according to your configured rules.

Now upload your documnts. Kudra AI processes each document automatically. Processing runs in the background while you continue uploading additional contracts or working on other tasks. There’s no need to monitor progress—the system handles everything automatically and delivers.

Transform Your KYC Process with Kudra

Regulatory pressure to maintain accurate, current customer information intensifies continuously. Compliance requirements evolve, fraud techniques become more sophisticated, and enforcement actions grow more severe. Manual remediation processes simply cannot keep pace with these demands.

We’ve explored how KYC remediation protects organizations from regulatory penalties, fraud exposure, and operational inefficiency. You’ve learned the tangible benefits automation delivers through improved speed, accuracy, compliance, and cost-effectiveness.

Now it’s time to experience these benefits directly. Kudra’s AI-powered platform is designed for customization to your specific regulatory environment, customer base, risk appetite, and operational constraints — whether you’re processing retail banking customers, corporate accounts, investment clients, or insurance policyholders.

Want to reduce remediation time by 90%, achieve near-perfect accuracy, ensure continuous compliance, and minimize fraud risk? Connect with our compliance automation specialists to discover how Kudra can transform your KYC remediation program.